See also

17.10.2025 06:11 AM

17.10.2025 06:11 AM

Once again, Friday's calendar contains very few macroeconomic reports. In earlier reports, we mentioned that there were no releases scheduled at all, but that isn't entirely accurate. Today, the eurozone will publish its second estimate for September inflation. However, this is a secondary report: second estimates almost always match the initial reading and are not marked as "high-impact." Beyond that, there are no notable releases scheduled in the U.K., Germany, or the U.S.

A number of fundamental events are scheduled again for Friday, but nearly all of them are insignificant in terms of market impact. This week saw at least 20 speeches from officials representing the European Central Bank, Bank of England, and Federal Reserve—but none of them delivered any market-shaking news.

As previously discussed, both Christine Lagarde and Jerome Powell have spoken regularly in recent weeks, giving the market a fairly clear understanding of where central bank policy is heading. The ECB has no intention of cutting rates, as there's currently no need for it. The Fed, meanwhile, appears likely to continue its easing path, as U.S. labor market indicators remain weak. It's also clear that the BoE will not pursue monetary easing in the near future, as inflation in the U.K. has been rising for over a year and currently exceeds the target level by nearly twofold.

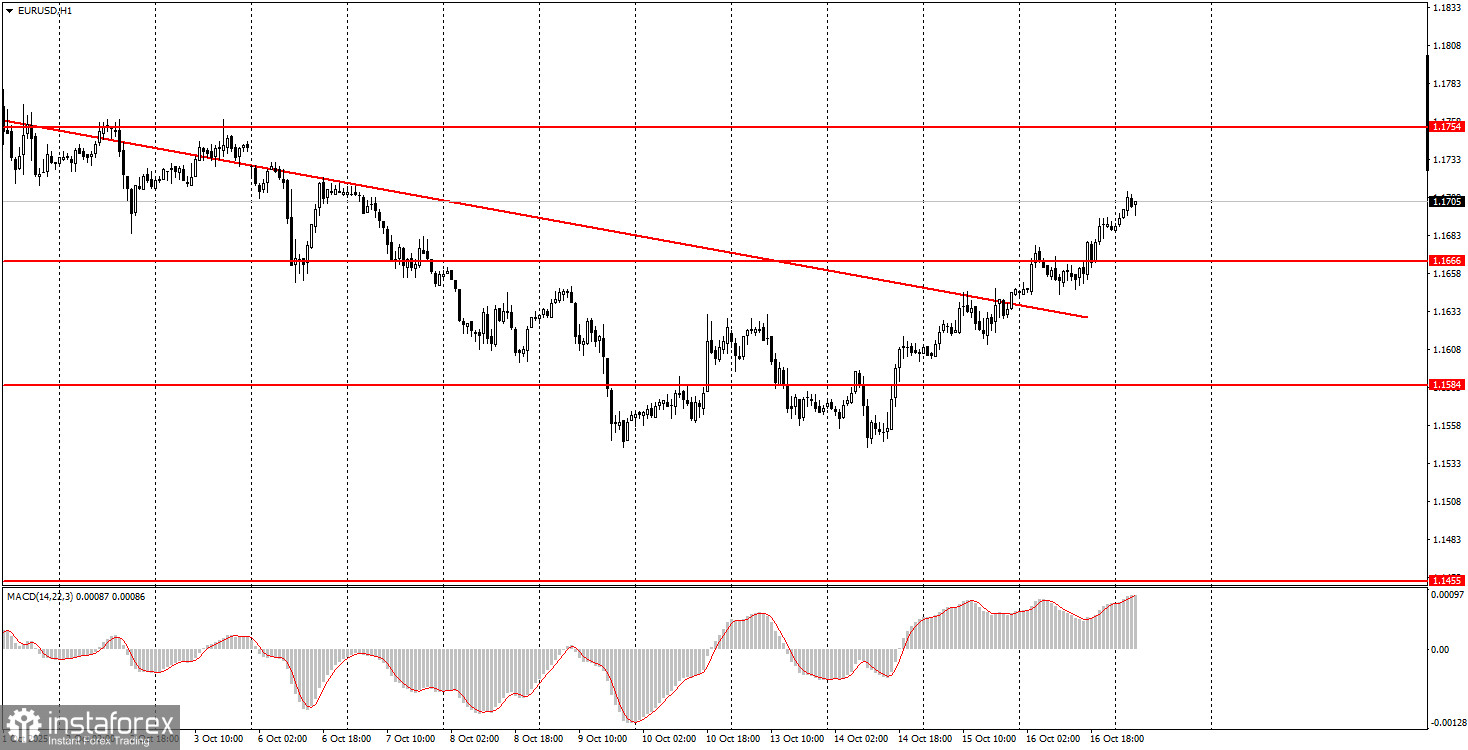

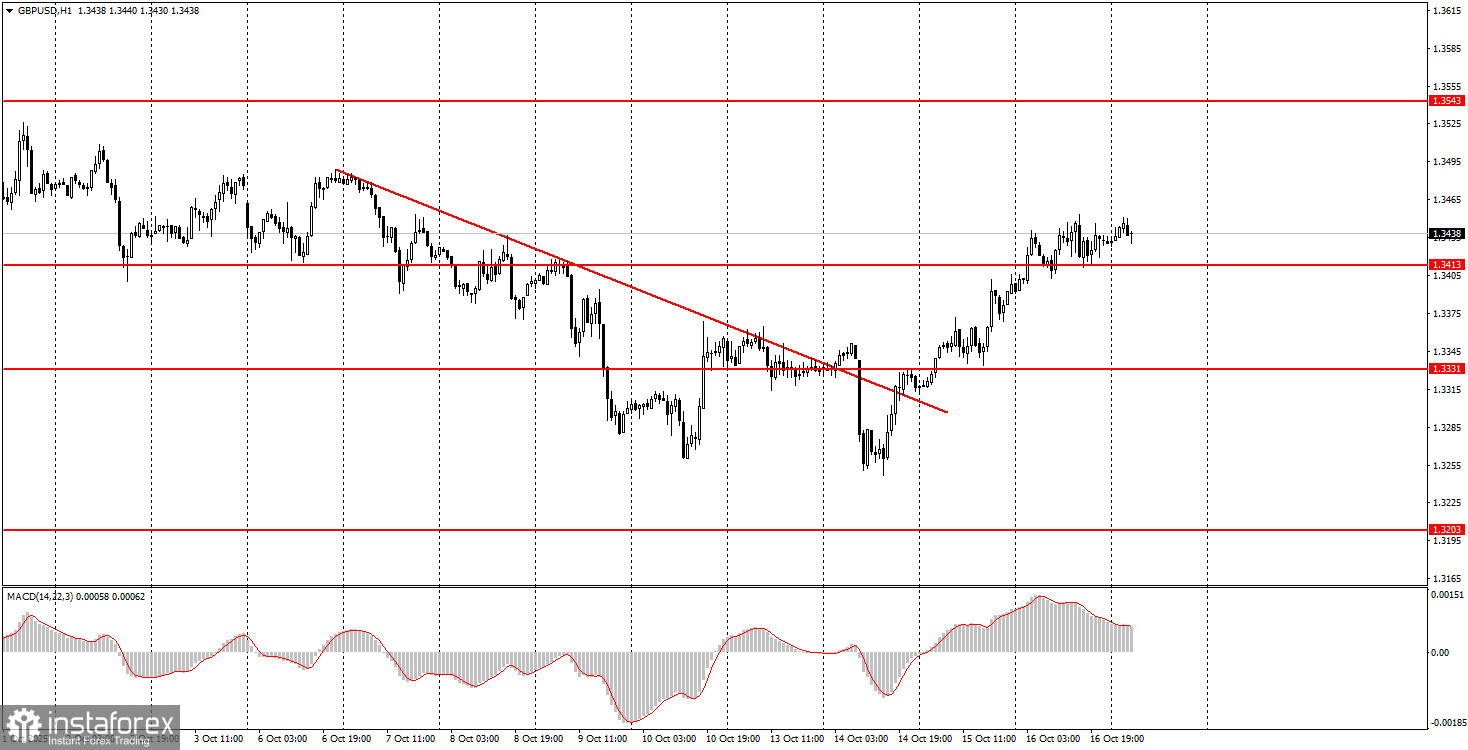

As we head into the final trading day of the week, both major currency pairs—EUR/USD and GBP/USD—may continue their upward movements, following recent breakouts above key trendlines. EUR/USD has completed a successful breakout above the 1.1655–1.1666 zone, making long positions still relevant, with room for further upward movement. In the case of GBP/USD, price action has also moved above the 1.3413–1.3421 zone, which opens the door for a rally toward the 1.3466–1.3475 area. With low-impact news expected and technical trends shifting upward, the focus remains on trend continuation for both pairs throughout Friday's session.