Vea también

01.07.2026 10:37 AM

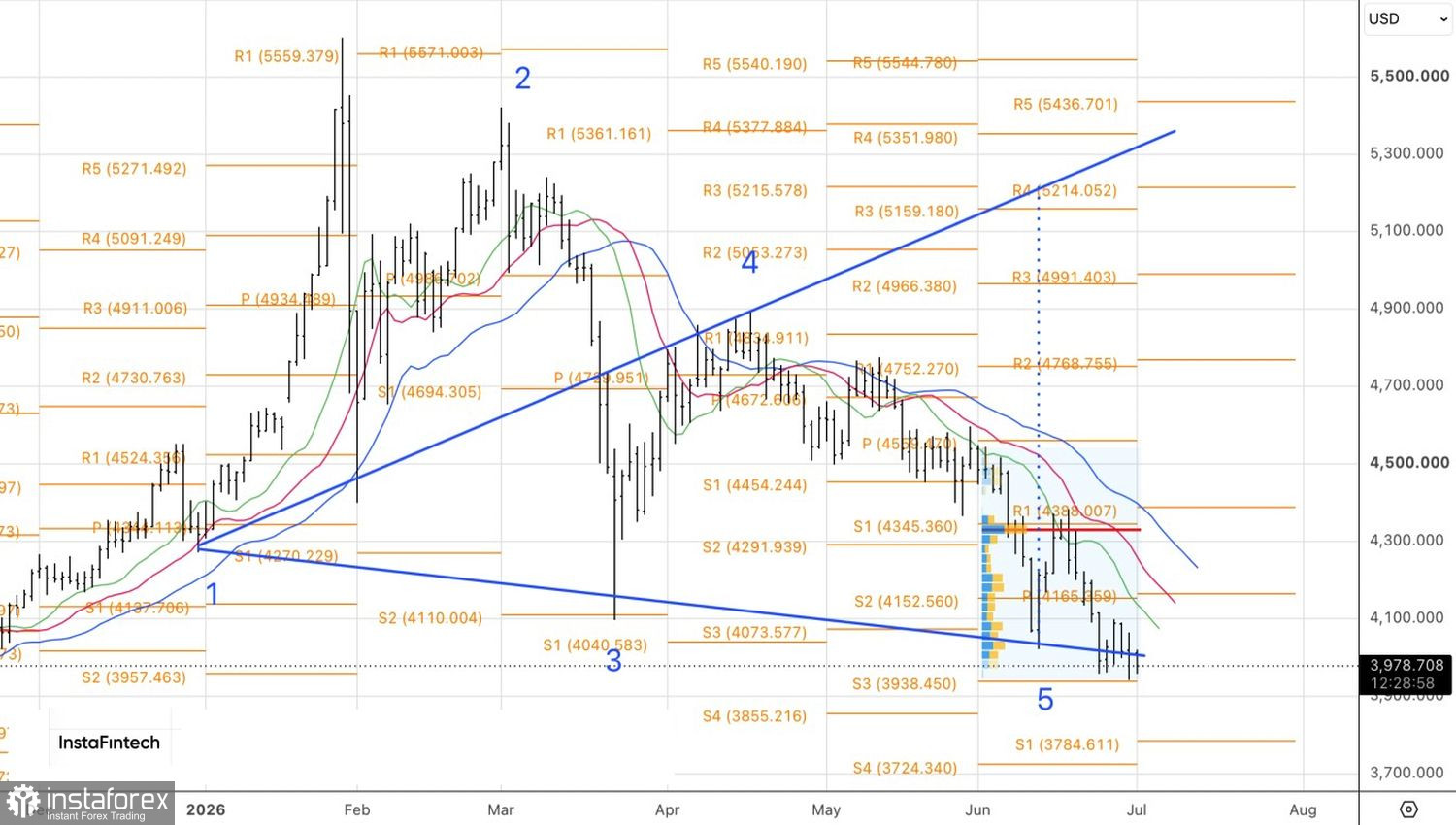

01.07.2026 10:37 AMGold has been too complacent, enjoying the title of the best asset of the year, to spot the approaching sell?off in time. The second quarter turned out to be the worst for the metal since 2013, driven by the Middle East conflict and the resulting surge in oil prices. A temporary US–Iran truce and falling Brent prices failed to help XAU/USD, as the futures market has increasingly priced in further Fed tightening.

Cleveland Fed President Beth Hammack said she does not see convincing evidence that current interest rates are restraining the economy and allowed that rate hikes may be needed to return inflation to the 2% target. The futures market now puts the odds of a September rate hike above 60% — the first time in three years that investors are pricing in higher, not lower, borrowing costs.

MUFG expects that lower energy prices, a strong dollar, and expectations of a longer period of higher interest rates will continue to weigh on the non?yielding metal. Labor market resilience only compounds those worries: strong May job openings gave the Fed room to act.

There is a less obvious driver behind the Treasury yield rally. Apollo Global Management says the AI capex boom is crowding US government debt out of the capital markets — hyperscalers are taking capital that once went into bonds. The question of "where will the hundreds of billions for buying new debt come from?" is becoming rhetorical.

S&P 500 vs. gold dynamics

The reversal is especially painful after the January rally to record highs. Gold has surrendered almost all its gains for the year and fallen below $4,000 for the first time in eight months. The S&P 500 denominated in gold turned up three months ago — roughly when Kevin Warsh was nominated as Fed chair, and markets began to doubt his dovish reputation. The "debasement trade" appears to have been losing steam even before the conflict wound down.

That said, the fundamental case for long?term demand remains intact. An OMFIF survey of 74 central banks found that 82% hold physical gold versus 71% a year earlier, and 30% plan to increase reserves over the next two years. Sixty?one percent expect a price of $5,000–6,000 by June 2027, and geopolitical risk as a motive for holding gold is mentioned 11 percentage points more often than in 2024.

JPMorgan argues that Warsh's hawkish communications have turned what looked like a pause within XAU/USD's structural bull trend into a deeper freeze: as long as the specter of rate hikes hangs over the market, investor engagement will remain very low.

Technically, the chances of Wolfe Waves forming on the daily gold chart have diminished but have not disappeared. For that scenario to be triggered, quotes need to return above $4,090/oz. If that happens, an Anti?Turtles pattern would be activated and provide a basis for buying.