See also

08.12.2025 12:54 AM

08.12.2025 12:54 AM

The German economy has been in a dire state for almost five years now. While "dire" may not be the most precise term, the reality is that the economy experiences periods of growth and decline. This is not what one expects from the "locomotive of the Eurozone." As the richest country in the bloc, Germany faces high expectations, and the last time its GDP grew by more than 1% year-on-year was three years ago—in the third quarter of 2022.

New Chancellor Friedrich Merz has taken steps to accelerate Germany's economic growth, notably by significantly increasing investments in defense and the military. These investments are being funded through increased public debt. However, the harsh truth remains—Germany is losing international competition and is currently unable to meet external challenges. Like the US, its labor is expensive, production is costly, goods are pricey, and taxes are high. China and other countries that were considered providers of cheap goods 20 years ago are not only catching up but are overtaking expensive American, German, and European products on the international market.

Of course, not all products can be substituted with Chinese alternatives. There are high-tech industries and categories of goods where quality and manufacturer reputation play key roles. However, each passing year demonstrates that high-quality products do not necessarily have to cost "as much as a Boeing wing."

The IMF believes that Merz's government will not be able to save the sinking German ship. According to the International Monetary Fund, the German economy needs significant structural reforms to stop losing the competition. Germany requires reforms both at the national level and within the framework of the Eurozone. Specifically, the IMF suggests reducing spending on social support, various subsidy programs, and tax breaks. In addition, there is a need to increase productivity and entrepreneurship levels. The IMF notes that Germany's industry is "stuck" and losing export competition to countries that are not stagnant and do not spend half their budgets on areas that can be abandoned painlessly.

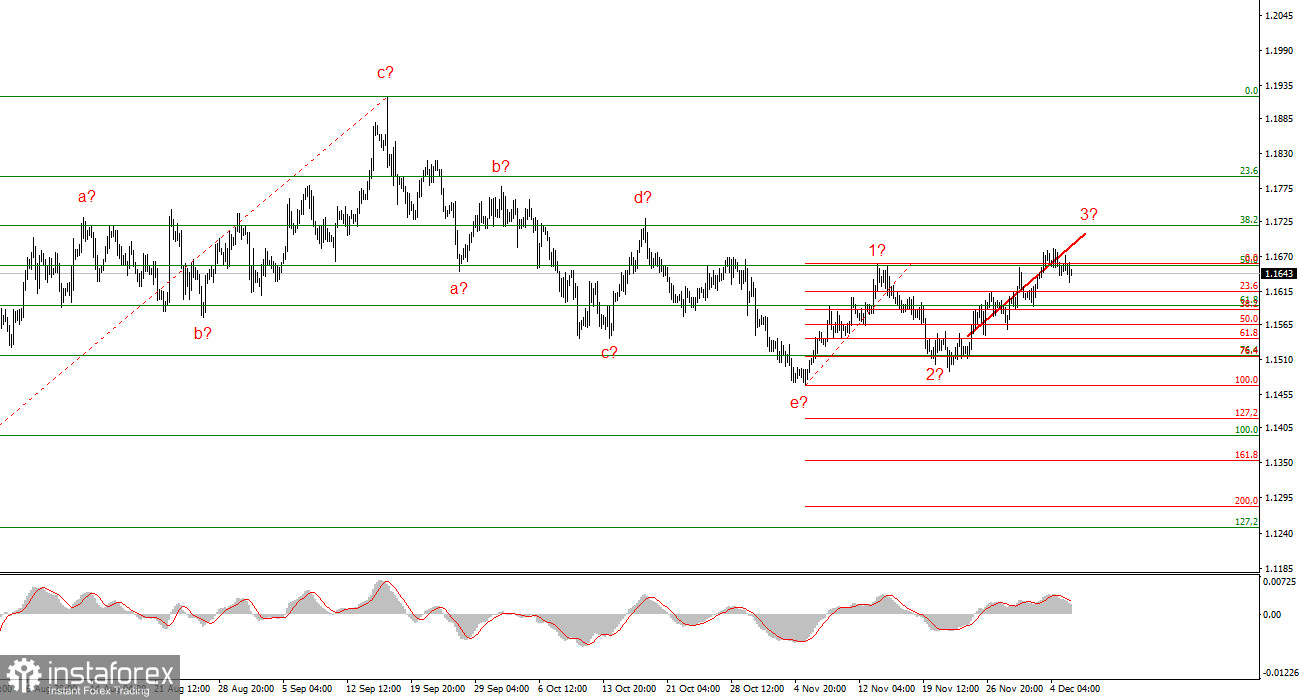

Based on the analysis of EUR/USD, I conclude that the instrument continues to build an upward section of the trend. The market has paused in recent months, but Donald Trump's policies and the Fed's remain significant factors in the US dollar's future decline. The targets for the current section of the trend could extend to the 25th figure. However, the latest upward section of the trend has again taken on a corrective appearance, so a downward wave may be starting within it, with a maximum leading to a new downward corrective set of waves.

The wave picture for GBP/USD has evolved. We continue to deal with an upward impulse section of the trend, but its internal wave structure has become complex. The downward corrective structure a-b-c-d-e in C in 4 appears quite complete. If this is indeed the case, I expect the main trend section to resume its build with initial targets around the 38 and 40 figures. However, wave 4 itself may take on a five-wave appearance.

In the short term, I anticipated the formation of wave 3 or c with targets around 1.3280 and 1.3360, corresponding to 76.4% and 61.8% Fibonacci levels. These targets have been reached. Wave 3 or C may continue its build, but the current wave set is likely corrective again. Therefore, a decline at the beginning of next week is also possible, and the attempt to break the 1.3360 mark has been unsuccessful.